There are two types of car title loans. Each of these loans work differently and include:

- Single Payment Title Loans

- Monthly Installment Title Loans

These two types of title loans work very differently and in this post we’re going over single payment title loans. We’ll cover monthly installment loans in another post.

Single Payment Title Loan Length

The first topic to cover is the length of the loan. Most single payment loans are for one month or 30 days. This is where the monthly interest rate came from and is still widely used today.

How the Loan Works

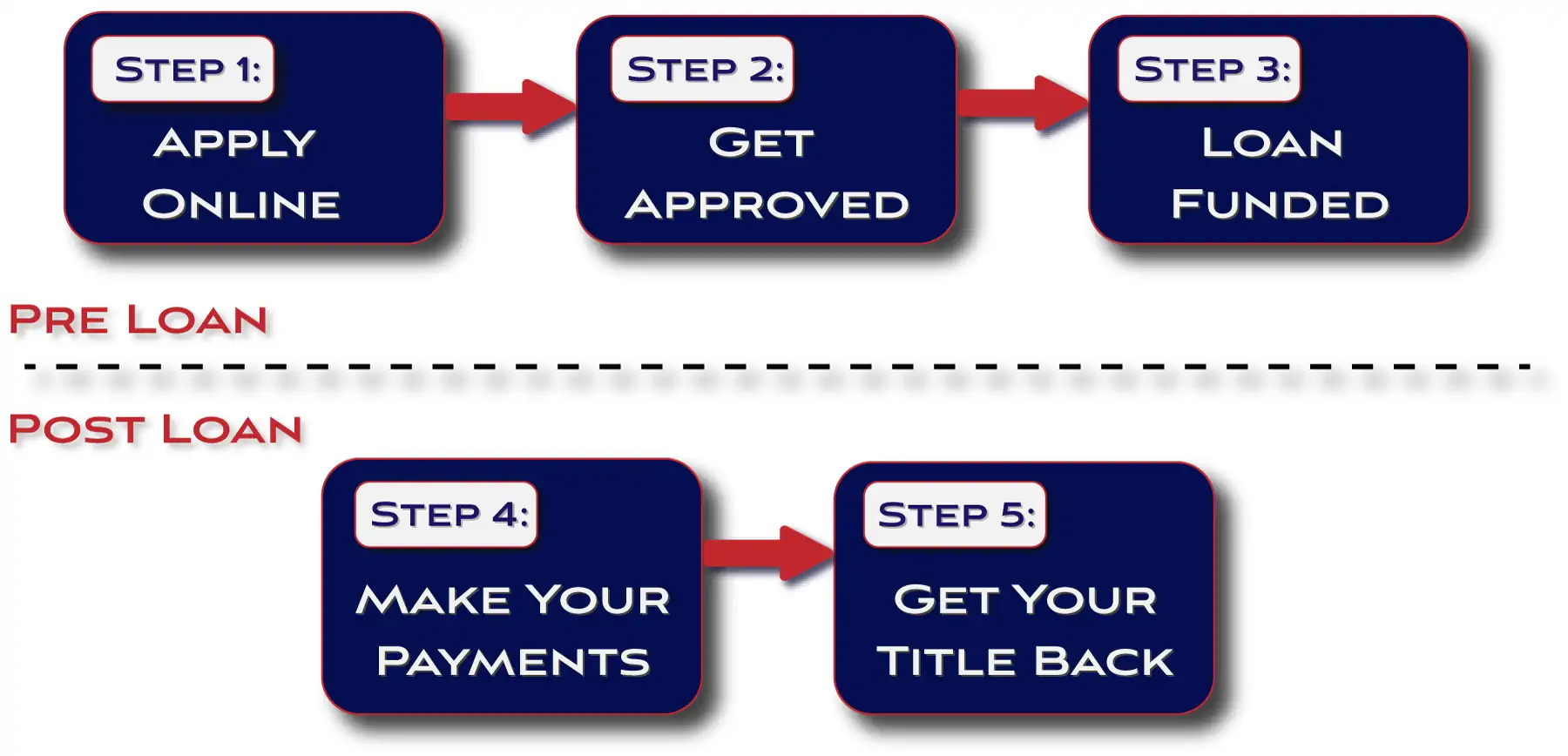

As we recommend preparation for any title loan is a critical step. We have published a number of suggestions of how to find the best title loan regardless of what type you are looking for. The process for the loan is the same as for any title loan, just with a single payment instead of monthly payments.

Apply

Once preparation is complete the next step is to apply. Applying for a title loan is easier today with more online options. Often the application process can be completed from the comfort of your home.

For completely online title loans the entire loan process can be complete from the comfort of your own home. This is especially true for no inspection and no store visit loans.

Get Approved

After completing your application the lender will follow up with any questions to fill in missing information. Then you will have your loan approved. The amount approved is base on the value of the vehicle.

Loan Funding

Following approval and completion of the loan agreement your loan is funded. This can be by check, direct deposit, cash, or debit card. The funding method depends of the lender and your preference.

Payment

Once the loan term is up you need to make your loan payment. For single payment title loans this is one payment due at the end of the loan. The payment includes the principal amount borrowed plus interest and fees.

Get Your Title Back

As soon as you make the loan payment you get your title back. This is the best part of a title loan because it is finished and you can move on having solved your short term financial problem.

Single Payment Title Loan Costs

A common question is how much do these loans cost? The true answer is it varies from lender to lender. The cost is a combination of interest and fees.

Interest Costs

Some lenders charge very high rates, some do not. Make sure to prepare properly and find a lender that charges reasonable interest rates.

Single payment title loans are calculated using the Monthly Interest Rate. This makes the interest costs fairly easy to determine.

Fees

The other part of the cost equation is fees. Some title loan fees are reasonable, some are not.

Total Cost Examples

The cost of a single payment title loan includes the following:

Fees + Principal Amount + (Principal Amount x Monthly Interest Rate)

Example 1

The first example we’ll look at is a $1,000 title loan for 1 month with a lien fee of $30 and an interest rate of 18% per month. If we plug these numbers into the equation above, we get the following:

Total Cost = $30 + $1,000 + ($1000 x 18%) = $30 + $1,000 + $180 = $1,210

Example 2

The first example we’ll look at is a $1,500 title loan for 1 month with a lien fee of $30 and an interest rate of 10% per month. If we plug these numbers into the equation above, we get the following:

Total Cost = $30 + $1,500 + ($1500 x 10%) = $30 + $1,500 + $150 = $1,680

Interest Rates Matter

Form the two examples above we can see that the interest costs for the $1,500 loan was actually cheaper to repay than the $1,000 loan.

Why? They both had the same lien fee and length. The reason is the interest rate for the $1,500 loan was 10% per month versus the interest rate of 18% per month for the $1,000 loan.

This is why preparing for the loan makes such a big difference in getting the best title loan. The lower the interest rate, the lower the total loan cost.

Other Vehicles – Motorcycles and Trucks

Truck title loans and motorcycle title loans work the exact same way as described above. The only difference is the type of vehicle used to secure the loan. Not all lenders provide loans on these vehicles, so check with your lender first.

What Happens if you make the Single Payment?

Single payment loans are often difficult to repay because the entire amount, plus interest and fees, is due within a month from the moan start date. Some borrowers have trouble making this payment given the size of the payment and the fact that they have only had one month to save the money.

In these cases the lender often ‘rolls over’ the loan for another month. This is not recommended for the primary reason that it can be very expensive. See what happens when you roll over a title loan.

Conclusion

As with any loan preparation should be a first step. Single payment title loans may be for a much shorter time frame assuming you don’ end up rolling over the loan. Find the best lender for your situation and always make sure to rea the loan agreement in fill before signing.