How much do title loans cost? There is no simple answer to this question. The fact is that title loan costs can and do vary widely based on a variety of different variables.

Regardless, it is important to note that car title loans are not low cost loans. Even the best title loans, including online title loans, are considered expensive when compared to most other loan types.

In some cases title loans can be very costly. It is important to do your research before getting one of these loans and find out exactly what you are committing to.

We have written several title loan cost and interest related posts. Some focus on how interest works, others on how extending the loan term can increase the total loan cost significantly. You can see this in real time using the car title loan estimate calculator.

The real answer to “how much do title loans cost” is: It depends. Not a great answer, but a truthful one. We’ll explain what exactly it depends on in the following sections.

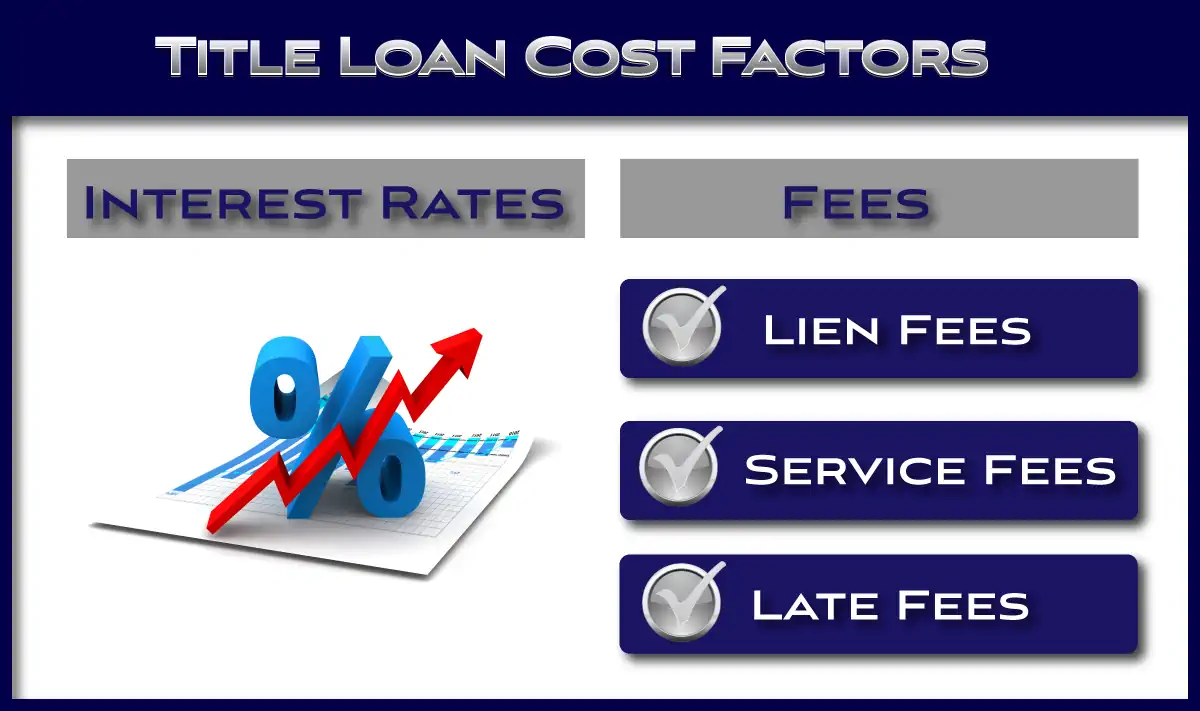

Title Loan Cost Factors

The reason the answer to “how much do title loans cost” is “it depends” is because of several factors. The biggest two are interest rates and fees.

There are other factors that do contribute to the cost of a title loan, but compared to fees and interest rates, for purposes of this post, we’ll consider them negligible.

Title Loan Cost Factor 1 – Car Title Loan Fees

The first category of costs that factor into title loan total costs are fees. The effect the fees have on the loan depends largely on where you get the loan and what type of fees that state permits.

Some states permit very few fees, others permit fees that make up the bulk of the loan cost. Finding this out is an important part of getting a title loan. It is critical to understand any and all costs associated with the loan before committing to one.

With some title loan companies this is easy. With many, however, it can be quite challenging to get an accurate title loan quote. This is part of preparing for the loan, a critical first step that we cover on our site.

Texas, for example, has loans structured with low interest rates to the actual lender. The title loan company, on the other hand, charges a fee for the loan that makes up the majority of the actual cost.

Types of Fees

There are multiple types of fees that can be related to car title loans. Some do and some do not have a major impact on the total loan cost.

Lien Fees

When you get a title loan, or any car loan for that matter, the lender records their lien on the title. There is a cost to do so and it varies depending on which state your vehicle is titled in.

The lender pays this fee to the motor vehicle department in that state, and usually adds the actual cost to the loan amount. Generally, lien fees do not have a major impact on total loan cost.

Monthly Service Fees

Monthly service fees are not permitted in all states. These fees can add a significant amount to the total loan cost. These are not common in every state, although some lenders in some states do charge a monthly service fee.

If the fee is a percentage of the total loan balance, it is essentially another way of charging interest. A 5% monthly service fee, for example, is like adding 5% per month the the interest rate.

Late Fees

The best way to deal with late fees is to avoid them. Make your payments on time and you will not have to worry about dealing with late fees. Making late payments can increase the total cost of the loan even if the late fee itself is not significant.

The principal balance usually continues to accrue interest. Making a late payment increases the amount of interest and, depending on how late the payment is, and how many times you make a late payment, can significantly increase total loan cost.

Title Loan Cost Factor 2 – Interest Rates

Car title loans, including online title loans, generally have a higher interest rate than many other loan types. The exception is payday loans which usually have a high rate. Even the best title loans can cost more than other types of credit such as a credit card cash advance.

Car Title Loan Interest Rates

The fact is interest rates for car title loans can vary widely. Some states have caps of 35.99% APR on all loans including title loans. Sometimes these loans have some other cost (like a monthly service fee or other fee) included in the loan.

On the higher end of the scale there are some title loans with rates of 25% per month, or 300% APR. In fact, if you read anything from credit card company affiliates like credit karma they make it seem like all title loans are 300% APR.

The truth is the average rate is somewhere in the middle. Just like most other topics in life, reality is in the middle of the extremes. There is, however, no getting around the fact that title loans are not inexpensive or low cost loans.

This does not mean that you should overpay for an online title loan. Finding a relatively low rate title loan, with an affordable payment, should be a goal when shopping for a title loan.

There is competition in the online title loan space. Where there is competition there are options. Find a solution that meets your needs at a cost that is affordable for you.

Amortization

Loan amortization is when a loan is broken into equal installments over a period of time. These installments are usually monthly. There are some online title loan companies amortizing title loans over longer periods of time.

Use some caution when trying to make a title loan a long term loan. They are meant to be short term solutions. Making a title loan too long can result in excessive total costs. Learn about how long you have to repay a title loan.

See some examples in our post on why title loans are not long term solutions.

Online Title Loan Considerations

The cost of a title loan theoretically should be the same for an in-person loan or an online loan. In some cases online title loans come with greater risk to the lender. This can result in two things occuring:

- A lower vehicle valuation. This can be somewhat anticipated, since the lender is making a title loan without seeing the vehicle. It makes sense that the vehicle value may be somewhat lower, and therefore the maximum loan amount somewhat lower.

- A higher interest rate. This is to make up for the actual or perceived increased risk. This is not always the case. If you are preparing for an online title loan this is one of the questions to ask.

Conclusion

How much do title loans cost? Well, the truth is it depends. Unfortunately there is no single answer to the question. You need to take into account all costs associated with the loan including interest rates and fees.

It is essential to get an estimate of the total loan cost, since title loans can be inclusive of both fees and interest. Each of these can make up a substantial portion of the loan costs depending on where you get the loan.

Questions:

In many states lenders are limited in the amount of fees they can charge, so most of the time the fee(s) charged will be capped and not excessive. This is not true in all states. For title loans in Texas, for example, some companies charge a “CSO” fee which equates to an APR of 200% or greater in many cases. Check with your lender and always find out total costs, inclusive of interest and fees, before signing any loan agreement.

Typically, like any other loan, a title loan will have a late fee. It is not uncommon to see late fees expressed as a percentage of the amount due. 5% is a common late fee; this means if you are late on a $200 payment, the late fee would be $10.

Yes, installment loans are usually amortized. This means you are paying a portion of the principal each month along with interest. With a single payment loan, you pay the entire principal, plus interest and fees, at one time.

The easiest way to save on a title loan is to find a lender with a reasonable interest rate that does not charge excessive fees. Find out the total loan cost before getting the loan in any case. If you already have a title loan you can save by making early payments, making extra payments, and paying more than the minimum each month. If the loan is a high interest loan every dollar and day count and can save you money.